- Home

Blog - Reviews

- News Letter

- Stop Foreclosure

- About Us

- What We Do

- Contact Us

- Foreclosure Defense

- Foreclosure Process

- Steps of Foreclosure

- Mistakes to avoid

- Short Sale Realtor

- Investment Property

- Buying Foreclosures

- DuPage Sheriff Sale Best Deal

- Will Sheriff Auction Best Deal

- Sheriff's Sale

- Sheriff Sale Rules

- Hardship letter

- Buying from Bank

- REO Properties

- Modification Approval

- Carol Stream RE

- Downers Grove RE

- Short Sale Purchase Timeline

- Rent Your Home

- House Financing

- Downsizing Your Home

- Mortgage Relief

- Loan Recast

- Links

- Pre-Approval Letter

www.LanaCole.net

SvetLana Cole - Full Time Licensed broker with "Charles Rutenberg Realty"

3135 Book Rd, Naperville, IL 60564

“Equal Housing Opportunity”

Cell 630-447-8382

Chicago Land Real Estate Monthly News Letters!

How to Pick the Best Short Sale Agent for a Brighter Future

Choosing the perfect short sale agent is crucial for a successful outcome. Don't solely rely on internet research and reviews. Instead, conduct face-to-face interviews, asking the right questions to gauge (GAGE) their expertise.

Beware of agents who claim to be experts and call them selves short sale queens and kings , but lack real experience in short sales. Look for a team of experts, including a knowledgeable agent, experienced short sale attorney, and reliable title company.

Ensure your agent is familiar with Equator, the platform used by major banks for short sales. They should know the different short sale types and attend the appraisal or BPO for your home.Be careful when agents promising cash incentives for short sales - they cannot guarantee that.

Empower yourself with knowledge. If you know more than your agent after watching my full version video, it's time to find a better fit.

Choose wisely and secure your financial freedom with the right short sale agent! Contact us for assistance and guidance.

Contracts outpace previous year's total

MRED's residential marketplace saw weekly and annual increases in listings under contract last week.

The 3,524 contracts marked a 41% week-over-week increase and a four-week high.

It was also a 7% year-over-year bump.

Time To Buy is Now!

Source {MRED MarketPlace}

3 Ways How NOT to loose your House!

1. A house can be lost in 6 months if HOA fees are not paid. Homeowners who live in a community with an HOA must pay fees to cover the costs of maintaining common areas and enforcing community rules. If a homeowner fails to pay their HOA fees, the association may foreclose, evict the owner, and seize the property.

2. A house can be lost in 6 months to a year to foreclosure. If a homeowner is unable to make their mortgage payments as promised, the lender will file a foreclosure lawsuit and take possession of the property.

3. A house can be lost in 2 years if property taxes are not paid. If a homeowner fails to pay property taxes on their home two years in a row, the local government will place a tax lien on the property. If the lien is not paid, the government will sell the taxes at a tax auction, and the property will be lost. The person who bought the tax lien will become the new owner of the property.

New listings dip for third straight week

(July 3-7 2023)

MRED's residential marketplace saw 4,744 new listings during the first full week of July, which included the holiday. That mark was a 4% week-over-week decrease and a 29% year-over-year decrease. This was the third straight weekly decline in that metric, which had just seen three consecutive weeks of increases.

What docs do I need for a short sale?

(Part 1)

To apply for a short sale, you need to gather several documents to put together an initial short sale package.

One - Hardship Letter: This letter explains your financial hardship and why you are unable to continue making mortgage payments. It should be signed and dated. Check out the Hardship Letter video below.

TWO - Authorization Letter: A signed letter giving permission to your lender to communicate with the real estate agent/attorney or any other authorized party involved in the short sale process.

THREE - Financial Statement form: This is a 2-page document that you will need to fill out, sign, and date. You can get this form from your attorney or realtor. It pertains to your assets, profit, and expenses.

Four - Three months of the most recent bank statements - ALL pages. You will need to submit all your bank statements. If you have any transfers of more than $150, you will need to write a separate letter explaining the source and reason for the transfer.

Five - Six consecutive months of pay stubs. If you are self-employed, then your W-2 or 1099 form and Profit and Loss statement should be signed and dated.

SIX - Two years of your most recent federal tax returns, including all supporting schedules and attachments. They should be signed and dated.

SEVEN - 4506-T form: Request for transcript of your tax returns. Your realtor or attorney can provide this form to you as well.

Eight - Your most recent mortgage statement for each of your mortgages, showing the outstanding balance of your loan, your loan number, and mortgage company contact information.

Home Inspection Tips for Buyers

Once the home inspection is completed, the buyer receives a detailed report outlining the property's condition, including necessary repairs or areas of concern. This information can be utilized in several ways: 1 Re-evaluating the purchase decision: If the inspection reveals substantial issues, the buyer may choose to back out of the contract. 2 Negotiating repairs with the seller: The buyer can request the seller to complete the required repairs before the closing. 3 Renegotiating the purchase price or requesting a credit: Alternatively, the buyer can negotiate a lower purchase price or ask for a credit to cover the cost of repairing the identified issues themselves. It is essential to hire licensed and qualified home inspectors to conduct the inspection. These professionals possess the expertise needed to evaluate the condition of residential properties accurately. By utilizing their services, buyers can make informed decisions and gain a better understanding of the home's overall condition, potentially avoiding unexpected and costly surprises after homeownership.

Who will pay the buyers agent in Illinois now?

Breaking news!

The real estate market in Illinois has experienced a significant shift in the payment of buyer's agent commissions.

The new approach places the responsibility of compensating the buyer's agent directly on the buyer, aiming to enhance transparency, align interests, and eliminate potential conflicts of interest.

These changes have the potential to reshape the dynamics of the real estate industry in Illinois, benefiting buyers by fostering a more client-focused and transparent home buying experience.

Traditionally, real estate agents in Illinois received a commission from the seller's side upon the successful completion of a home sale.

This commission was typically split between the listing agent (representing the seller) and the buyer's agent (representing the buyer).

However, the updated regulations have introduced a fresh perspective by shifting the responsibility of the buyer's agent's commission to the buyer themselves.

Under the new guidelines, buyers now have more control over the payment of their agent's commission.

How is this for a NEW Rule?

Market heats up with summer as contracts reach yearly high

(6/12 to 6/20 2023)

The number of homes under contract across MRED’s service area reached the highest level of 2023 for the week ending June 20, with 3,943 properties recorded as being in contingent, closed or pending status. That’s a 9.6% increase over the week of May 22, which saw the second highest number of under contract listings.

Source {MRED marketplace}

Real Estate Market Update - Free Money VS Inflation

In 2019, house prices and interest rates were low.

In 2020, prices remained low during the COVID-19 pandemic, and interest rates dropped, making it a great year to buy.

In 2021, prices went up, and interest rates started to rise, but rent prices increased even more, making it still a favorable year to buy.

In 2022, prices and interest rates rose quickly.

Currently in 2023, prices and interest rates are stable, but rental prices are increasing along with inflation.

The printing and distribution of free money by the government significantly influences home prices and prices in general, driving inflation. The majority of this free money has ended up with the ultra-rich, who are investing their surplus wealth mainly in real estate, causing home prices to rise. Increasing interest rates limit the amount of money people can borrow for buying homes, reducing their affordability. Borrowers now face competition from cash buyers, particularly the ultra-rich.

Cash buyers are unaffected by rising interest rates. This explains how the printing and distribution of free money leads to higher home prices and decreased affordability.

Individuals are finding it more challenging to afford homes, and even large companies that rely on borrowed money for real estate operations are facing difficulties due to higher interest rates.

While this exerts some downward pressure on prices, we believe it will not be sufficient to decrease residential real estate prices in the coming year. We expect prices to stabilize near their current levels while wages increase in the coming years, counterbalancing the reduction in money printing. In other words, we anticipate no reason for home prices to decline and rather expect them to continue increasing at a historical pace in the future

#realestate #realtor #freeMoney #inflation #colelanaRealtorNaperville #napervilleRealtor #downersGroveRealestate #downersGroveRealtor #timeToSell #lowInventoryHomes #perfectTimeSellHouse

5 Tips for a Stress Free Closing

Median home prices record best performance of year

(May-June 2023, Real Estate market Update)

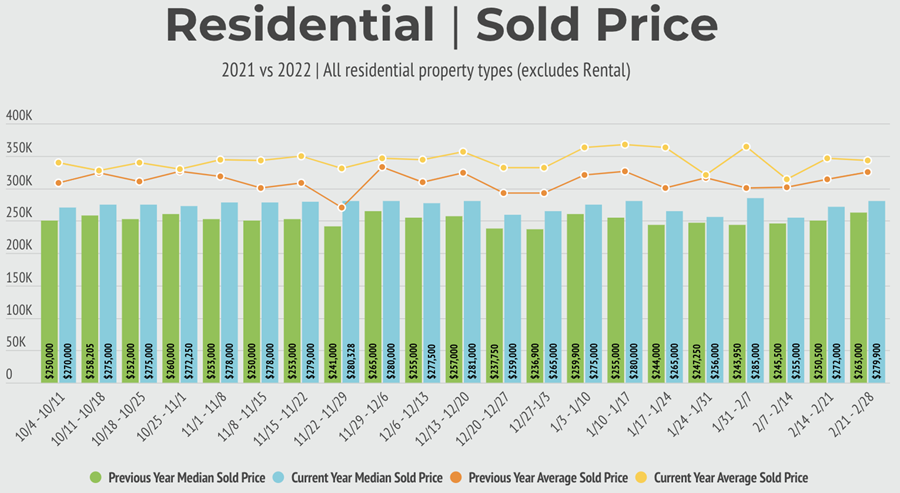

Median prices for residential properties in MRED's connectMLS reached their highest point this year in the week ending June 4. The median price of a home was $327,000, a 7.2% increase over the previous week and a 2.2% gain over the median price for the same week in 2022.

Source {Mred MarketPlace}

#realestate #realEstateUpdate #MarketPlace #Realtor #coleLanaREaltor #realestateagentDownersGrove

#TimeToBuy is NOW!

Contracts narrow year-over-year gap

Last week's 20% rise in residential listings under contract in MRED's marketplace ushered in the largest single-week contract total since late August. That increase also narrowed the year-over-year gap to a 3% annual decrease, the smallest margin in three months.

Source (MRED data)

#TimeToBuy is now!

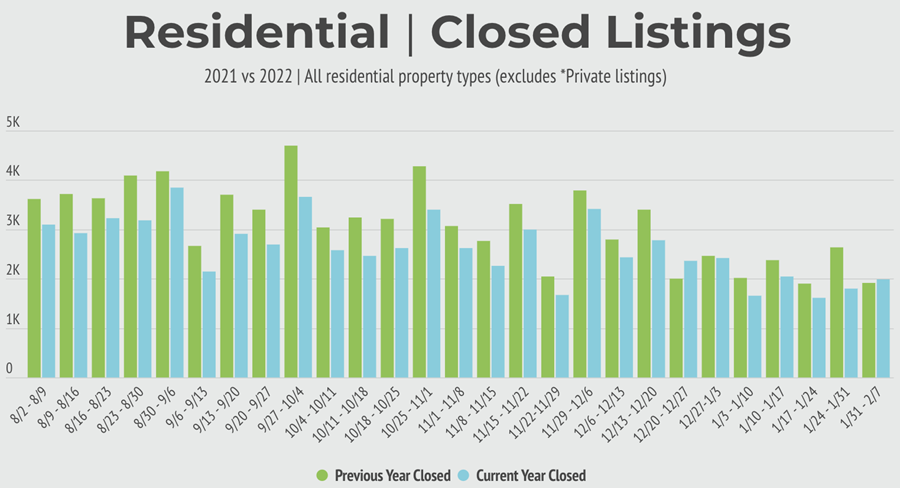

Closed listings rise for second straight week

(1/30 to 2/6/2023)

A total of 1,345 residential listings closed in MRED's marketplace last week.

That tally marked a 17% week-over-week increase and the second consecutive week of gains in that metric.

Despite the bump, the 2022 mark from the same period still bested this year's total by 42%.

Source (MRED data)

#TimeToBuy is now!

Median sales prices spike

(1-16-2023 to 1-23-2023)

Residential sales prices in MRED's marketplace have begun heating up this winter.

Last week's $275,000 median sales price was a 6% increase on a weekly and annual basis.

It was also tied for the highest mark since early November.

Source (MRED data)

#TimeToBuy is now!

Residential median sales price increases

The median residential sales price in MRED's marketplace increased 2% on a week-over-week basis during the Dec. 12 to Dec. 19 period. That same span also marked a 2% annual decrease heading into the final full week of 2022.

Source (MRED data)

#TimeToBuy is now!

Is Real Estate market turning around again?

Residential contracts see second weekly jump.

Contracts in MRED's residential marketplace increased by 9% on a week-over-week basis during December's first full week.

It was the second week in a row that contracts increased after a holiday decline.

Despite the rebound, this total still fell 27% short of the total from the same span in 2021.

Source (MRED data)

#TimeToBuy is now!

Current Mortgage Rates

(Dec 1-7/22)

Thank you to AandN mortgage for providing us with weekly mortgage rates.

{Source A&N mortgage rate}

Closed listings mark nine-week high

(Oct 28/22 - Dec 5/22)

MRED's residential marketplace saw 2,369 listings close last week.

Not only was that a 104% week-over-week increase from the previous holiday week, it was also the largest total since the start of October.

Thank you to MRED!

MRED data source

#TimeToBuy is now!

Naperville Data - November of 2022

Here are the latest housing market statistics for Naperville, IL! If you'd like more detail on the market, what's available or how much your home might be worth, let's set up a meeting to discuss! #houseexpert #housingmarketexpert #house #home #listreports #localhousingdata #areaexpert #realestate #realestateagent #househunting #homeowner #hometrends #housingtrends

Holiday week continues year-end inventory dip

(Nov 30/22)

The Thanksgiving holiday brought about a predictable slow down in several market indicators.

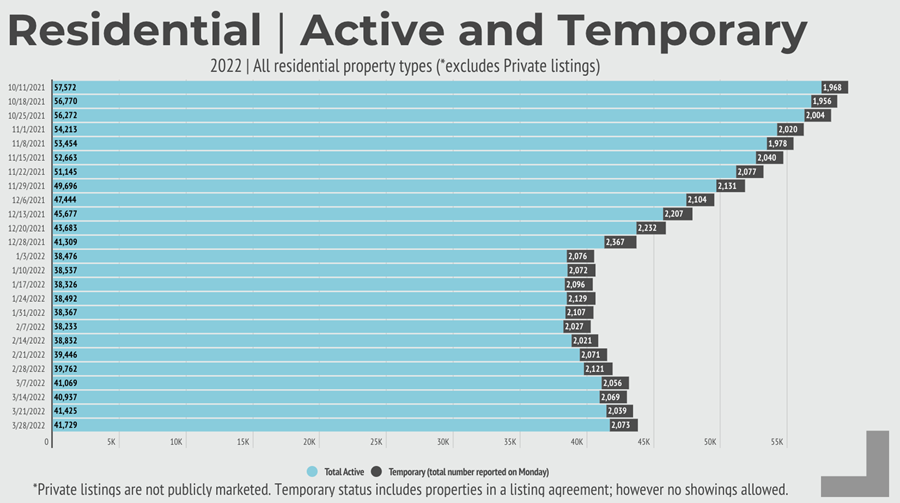

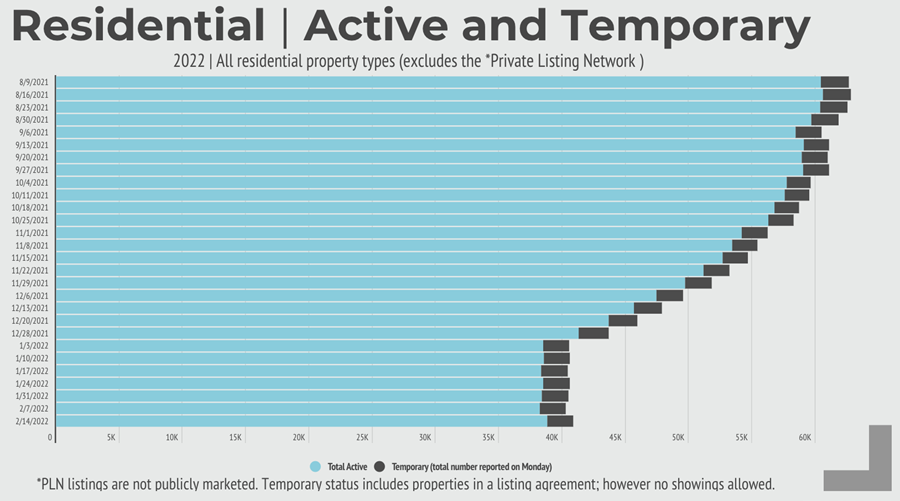

Residential active listings decreased on a week-over-week basis for the 10th straight week, with 42,573 listings active in connectMLS.

Data source {MRED marketplace data}

Let's fill in winder inventory! #TimeToSell is now!

New listings continue to decline.

(Oct 2022)

New listings continue end-of-year decline

The final week of November saw 4,527 residential listings added in MRED's marketplace.

That total was a 2% week-over-week decline and a 12% annual dip.

It also marked the lowest single-week total since mid February.

Data source {MRED marketplace data}

#TimeToSell is now!

Open House Increase - means Buyers market!

(October 2022)

Nearly 3,000 open houses hosted.

MRED's data shows 2,997 residential open houses last week.

That total was an 8% week-over-week increase.

It was also the second-largest weekly open house total of the last three months.

Data source {MRED marketplace data}

Multiple offers OVER asking price are in the past?

#TimeToBuy is now!

New listings reach nine-week high

(Oct 3 - Oct 10)

New residential listings in MRED's marketplace registered a 3% week-over-week increase during October's first full week.

This bump marked the first time since mid July that new listing totals rose in two consecutive weeks.

Last week's total still fell short of last year's mark during the same span by 8%.

Data source {MRED marketplace data}

#TimeToBuy is now!

End of September Dip

(9/19 - 9/26,2022)

Closed listings dip on weekly, annual basis

The number of closed residential listings in MRED's marketplace registered week-over-week and year-over-year declines during September's final full week. A total of 2,118 listings closed last week, compared to 3,274 during the same span in 2021, a 35% drop.

This number was also a 6% weekly decrease.

Data source {MRED marketplace data}

#TimeToBuy is now!

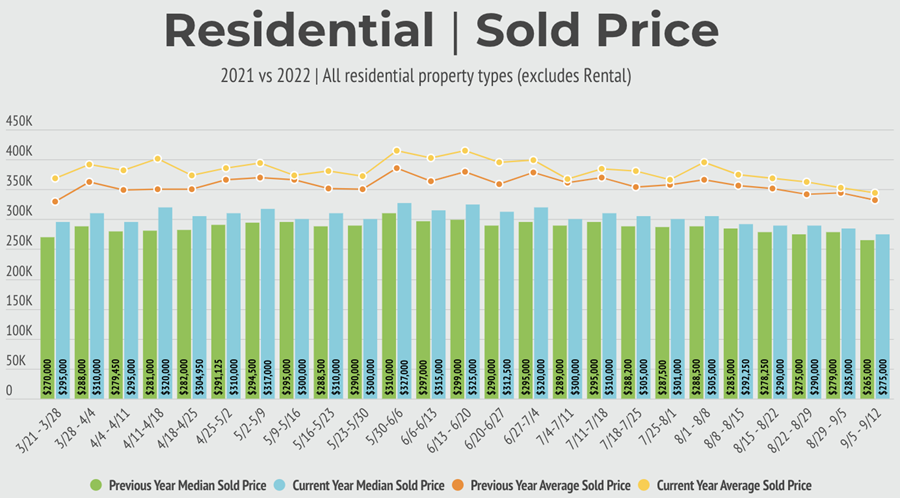

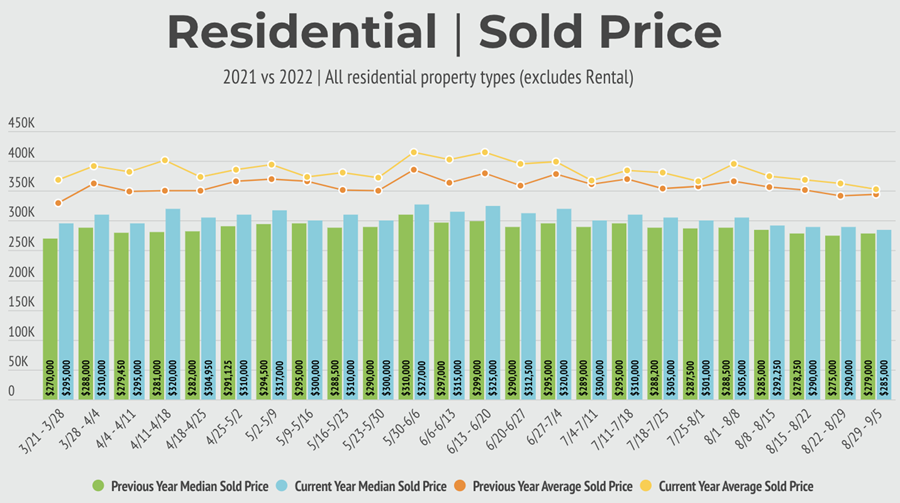

Median sales price at lowest point since February

(9/5 - 9/12)

After five straight weeks without an increase, the median sales price among residential listings in MRED's marketplace reached a seven-month low.

The $275,000 mark is the result of a 3.5% week-over-week decline, but still outpaces 2021's total in the same period by 3.7%.

Data source (MRED marketplace data)

#TimeToBuy is now!

Closed listings approach low point of 2022

Only 1,840 listings close

9/5 to 9/12/22 data

The first full week of September saw fewer closed residential listings in MRED's marketplace than any week since January.

The 1,840 closings were a 42% week-over-week decrease and a 32% annual dip as fall approaches.

Source {MRED marketplace}

Great News!!!! Almost NO competition !

#TimeToBuy is NOW!!!!

Median sales price reaches five-month low 8/29-9/5-2022

The median sales price in MRED's marketplace fell 2% week-over-week, continuing a month without any increases in this indicator. The $285,000 median sales mark was a 2% annual increase, but the lowest in 2022 since early March.

Source {MRED marketplace}

#TimeToBuy is finally NOW!!!!

Housing Recession?

&

Is Lowballing Back?

(August 31/2022)

More signs are pointing to a housing slowdown as existing-home sales—completed transactions for single-family homes, townhomes, condos and co-ops—fell 5.9% month over month and 20% year over year, according to the National Association of REALTORS®’

Probably the most painful part of buying a home today is the price you pay—which has shot up over the past year by 16.6%, to a national median of $449,000.

But there’s also good news for homebuyers still hanging in there: Houses that were once snapped up in record time are starting to linger longer on the market.

The number of homes with price cuts increased to 19.1% in July of this year, compared with 9.4% at the same time last year.

In other words, the red-hot seller’s market of the past two years is at long last cooling off, and some sellers fearing they’ve missed the peak of the market are desperate to unload their home before things get worse.

This means some brave homebuyers might find themselves in a unique position where they could (gasp) offer below the list price—otherwise known as lowballing.

Why lowballing is on the rise today

No more hundreds of buyers flocking to your Sunday-fun-day open houses.

What’s changed post-pandemic is that buyers are expecting truth-telling inspections again, and they are not buying sight unseen or overpaying any longer.

In other words, buyers just aren’t putting up with home sellers’ inflated prices anymore. And one way they communicate this line in the sand is with a lowball offer below the list price.

When to lowball on a house

Lowballing below the list price makes sense in a few scenarios:

- The house has been on the market for a while.

- The house is overpriced for current conditions.

- The house is in poor condition and will require extensive repairs.

- The house has issues like a bad location or a strange layout.

- The sellers are eager to sell and have a tight timeline.

Other things to keep in mind when making an offer below asking price:

- Have your financing in order so you can include a mortgage pre-approval letter from a lender.

- Consider minimizing contingencies. But be careful which contingencies you remove.

- Be prepared for a counteroffer and how you will handle it. Consider including an escalation clause.

- Increase the amount of your earnest money deposit.

Source {Realtor.com}

#TimeToBuy is NOW!

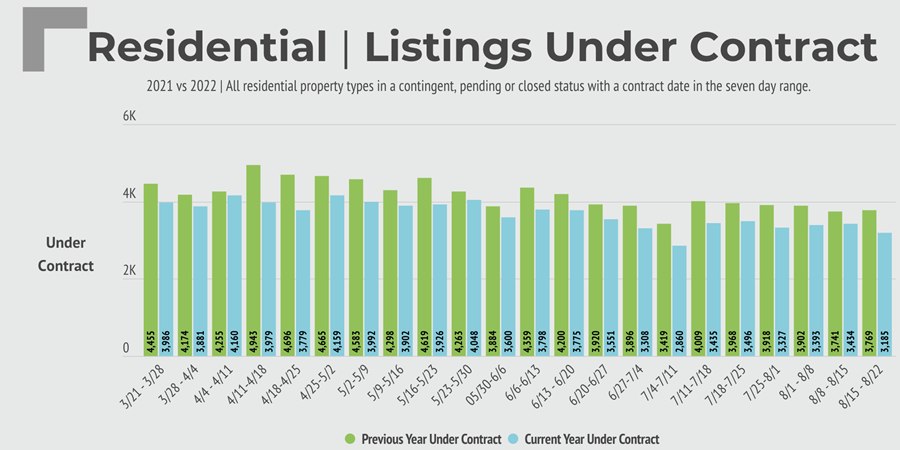

Marketplace metrics dip across board

August 15 - August 22

Listings under contract showed the largest dip with a 7% week-over-week drop.

The 3,185 contracts last week was the lowest since early July and second-lowest since February.

Source {MRED marketplace data}

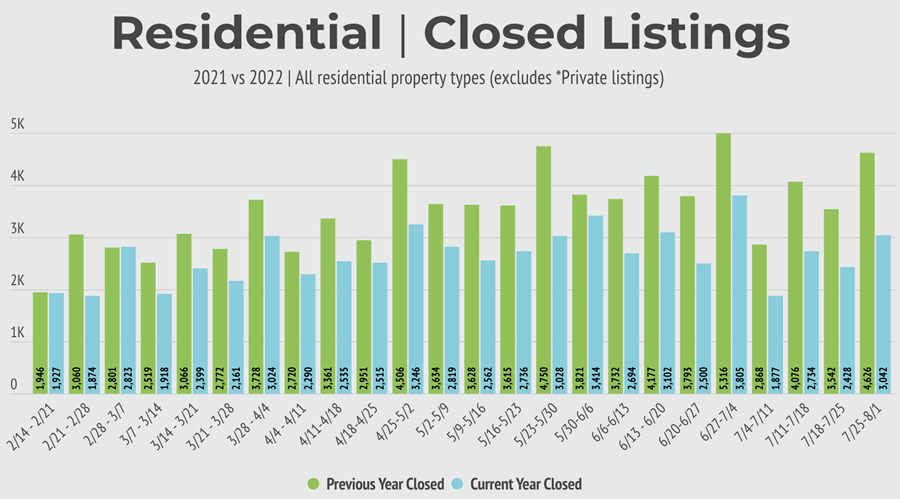

Closed listings are up, but still short of 2021

July 25 through August 1st

MRED's marketplace saw its usual end-of-the-month increase in closed listings to round out July.

The 25% week-over-week bump to 3,042 closed listings was still 34% shy of last year's total during the same span.

{Source MRED marketplace data}

New listings down on weekly, annual basis Report

July 18 through July 25/2022

New listings in MRED's marketplace fell 7% week-over-week.

That weekly decrease accompanied an 18% annual decline in the same metric.

That's the largest annual new listings decrease since early March.

Source {MRED marketplace}

New Listings Stabilize at Highest Point this Year

May 2-9

This week, the number of new residential listings in MRED's marketplace eked out a new high for 2022:

- New listings this week: 6,555

- New listings last week: 6,554

- Year-over-year change: -16%

Source {MRED data}

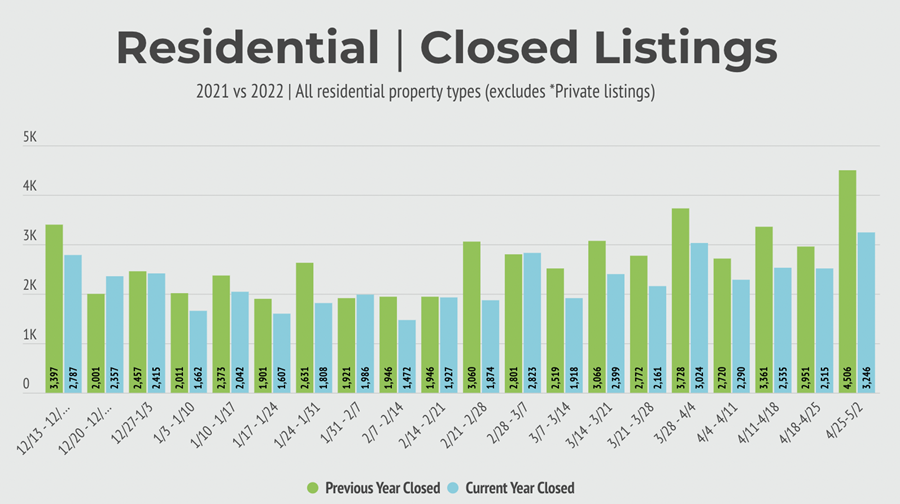

Downshift in residential closed listings extends into May

4-25 to 5-02 2022

Despite a 29% week-over-week increase in closed listings among MRED's marketplace, this week's residential closed listings remained significantly lower than last year:

- Total annual closed listings as of this week: 3,246

- Total annual closed listings as of last week: 2,515

- Total annual closed listings as of this week last year: 4,506

- Week-over-week change: +29%

- Year-over-year change: -28%

Source {MRED data}

Thank you MRED!

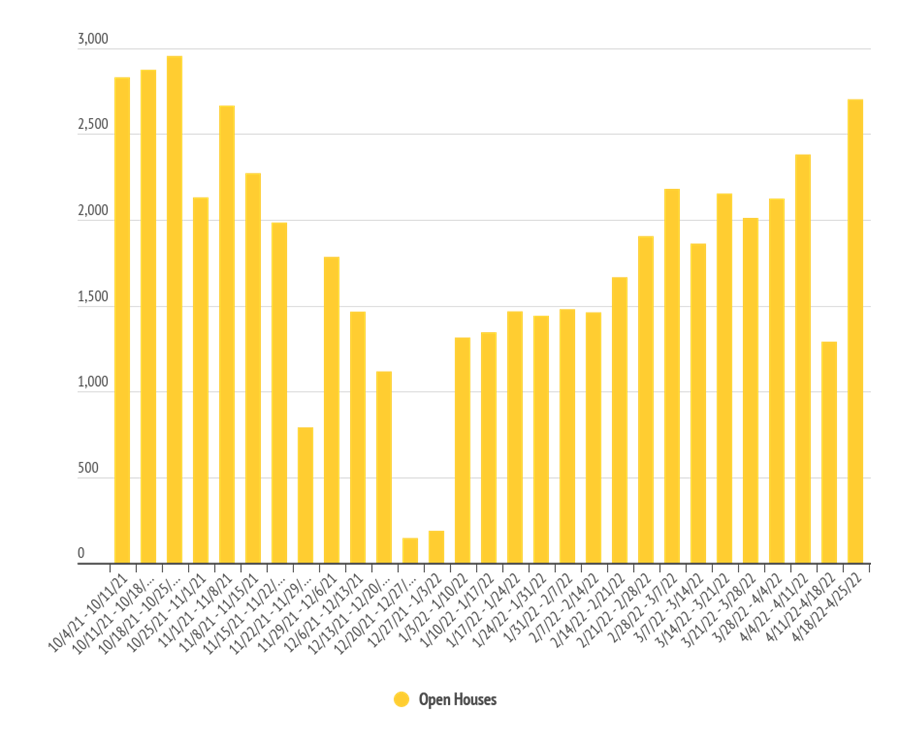

Big leap in open houses this week

(4-18-2022 through 4-25-2022)

Spring has sprung and so have eager home sellers. The number of open houses among MRED marketplace’s residential listings reached their highest number since October 2021:

- Open houses last year: 2,504

- Open houses this week: 2,703

- Year-over-year increase: 8%

{Data Source - MRED}

#TimeToSell is now!

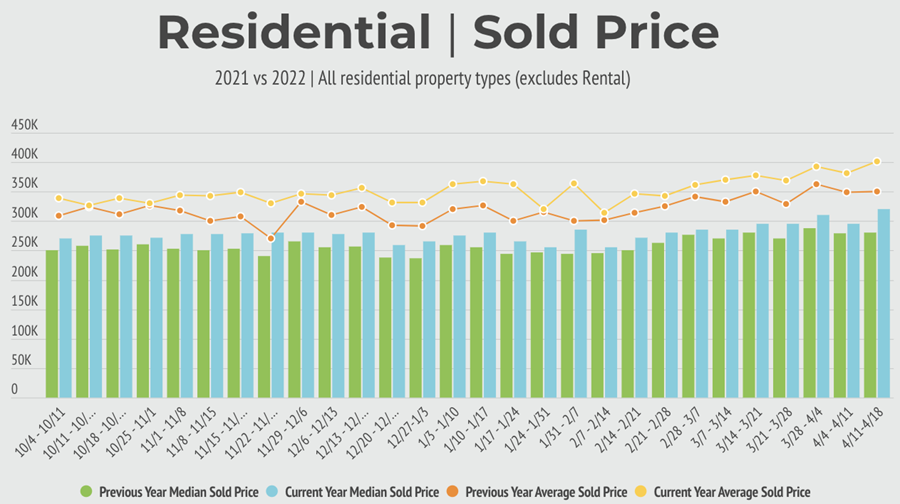

Median sales price reaches new peak as of April 18/2022 Are we in RE Bubble?

The median sales price among residential listings in MRED's marketplace hit a new all-time high in April's second full week:

- MRED marketplace residential median sales price: $320,000

- Week-over-week increase: 8%

- Annual increase: 14%

Source {MRED Weekly Market Snapshot}

Major Factors that Affect Real Estate housing market

Multiple metrics hit high point of year

"Listings under contract reach eight-month high"

The first full week of April ushered in 2022 peaks in several key metrics. Listings under contract, new listings, total active listings and open houses all topped their previous 2022 highs across MRED's marketplace. Most notably, contracts jumped 7% to 4,160.

Source {Weekly Market Snapshot by MRED}

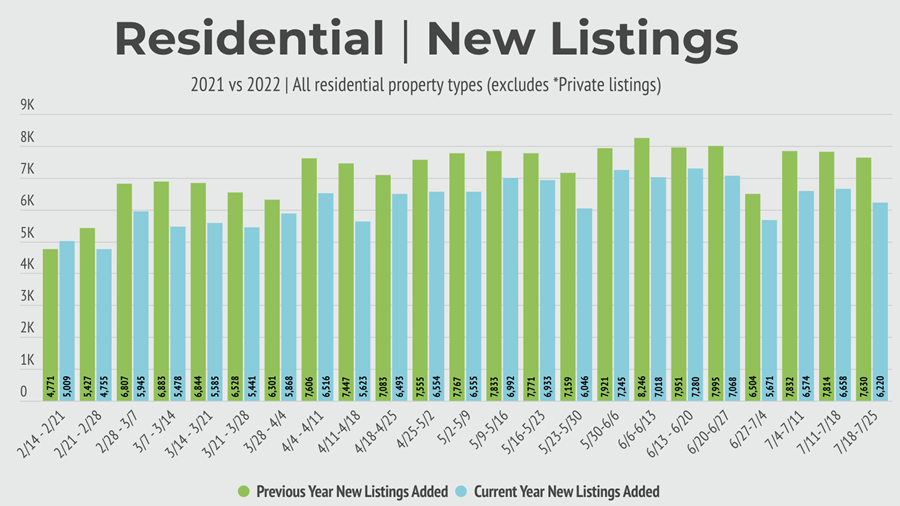

New listings spike to second-highest point of 2022

(1st week of April data)

Surge in listings seen as Spring market heats up.

Last week saw an 8% week-over-week increase in new listings across MRED's marketplace.

This bump brought on the second-most new listings in a single week since the new year began.

The 5,868 new listings fell 7% short of that metric in the same span from the previous year.

Thank you MRED for "Weekly Market Snapshot"!

Source {MRED}

#TimeToBuy is now!

Listing total hits three-month high

More than 41,000 active listings were available across MRED's marketplace during the final full week of March, the most since mid December. The 1% week-over-week increase continued the gradual rise leading up to spring market.

Source {Market Snapshot}

Listings under contract keep rising

March 7-14th

MRED marketplace sees four-month contract high

Residential listings under contract in MRED's marketplace saw a 4% week-over-week increase.

The 3,827 contracts is the most in a single week since November but a 13% annual decline.

Source {MRED Marketplace data}

Crazy Spring Real Estate Market!

"Biggest 8 mistakes Sellers make in this crazy sellers market "

Did you know the housing market is a sizzling seller’s game at the moment, where homes stand to spark bidding wars and sell for sky-high prices.

“COVID-19 caused so many people to re-evaluate their shelter needs, resulting in increased demand for homes and a continued lack of inventory,” explains Lindsay Reishman, founding partner at The Reishman Group in Washington, DC.

All in all, this is great news for sellers—yet with soaring prices and high expectations come a whole new set of possible pitfalls that could trip up inexperienced sellers, particularly if they’re selling for the first time.

Curious how you might risk ruining a good thing?

Here are 8 points for you to identify what many first-time and not only home sellers get wrong when listing their home today.

1. Overpricing your property

Just because sellers dominate now, don’t think “red-hot market = super high list price.”

A smarter strategy is to list lower than your goal and let the market do its magic.

“First-time sellers often erroneously believe that the list price means the desired purchase price,” Reishman says. “In fact, the list price simply indicates an approximate appropriate price, and its purpose is to drive interest in the property.”

The greater the interest, the more likely the price will climb as eager buyers bid on it.

You’re more likely to get interest with a lower asking price.

2. Skimping on home showings

In our not-quite-post-pandemic era, some homeowners may list their property, then feel skittish about having strangers traipse through.

To cash in, however, you can’t wait it out.

“As soon as the house is listed, it’s vital to allow as many qualified buyers view it as possible, to help build demand,” says Jonathan Faccone, managing member of the Halo Homebuyers company, based in Bridgewater, NJ.

“A seller has a fairly short time window to do this effectively, since if the house sits on the market, buyers may assume something is wrong with it.”

If you’re truly uncomfortable with in-person showings or have serious scheduling conflicts, virtual tours may separate out looky-loos from truly interested parties.

Then, once you know you have a prospective buyer who loves your listing, you can have them scheduled for a (masked) showing.

3. Staging slip-ups

With houses selling so fast, you may think you needn’t bother with professional staging. Still, if you want to fetch that dream price that you’ve heard is within reach, it could pay to present your home perfectly, with some professional home-staging help.

“In my recent experience, staging can reduce a property’s time on the market considerably and have a 1% to 5% increase in value offered by buyers,” says Stephen Keighery, CEO of Home Buyers Louisiana.

Today’s market is keeping these interior design pros busy—as in booked solid for months in advance. So plan ahead.

4. Seeing only dollar signs

A big payoff is tantalizing, but money isn’t everything.

“Many people look at price as the end-all-be-all, but a smart seller considers a variety of factors to make an educated decision,” says Aaron Carroll, a real estate agent at Douglas Elliman in Dallas.

“For instance, the highest offer may have a loan with an appraisal contingency, while a somewhat lower offer might be in cash.”

Perhaps the bidders with the highest offer need to sell their home first. That could mean a slow or snag-filled deal. You might be better off taking a slightly lower offer.

5. Pouncing on an implausible offer

Guess what: Buyers know it’s a seller’s market too, so some may make ginormous bids to beat out the competition—offers that can fall apart in financing or upon appraisal or inspection.

“In this market, it’s not uncommon for a buyer to submit an offer for a home, sight unseen,” says Deborah Ann Spence, a broker at Fierce Real Estate Corp. in Bala Cynwyd, PA.

“Then, if the buyer doesn’t like what he eventually does see, the offer can be withdrawn, and the property is likely to lose traction.”

The takeaway? If something seems too good to be true, it usually is! Work with your real estate agent to understand who is bidding and how serious they are, to avoid having your deal unravel.

6. FSBO blunders

While “For sale by owner” sounds like a direct route to extra profit, cutting brokers out of the picture is a risk.

“Today’s rookie sellers may be tempted to try selling their house on their own,” says Faccone, to save the agent’s commission. “But doing so severely limits your exposure.”

FSBO homes, after all, can’t be listed on the Multiple Listing Service, which is where most buyers shop for homes. And this exposure is crucial if you want to reach a large audience and fetch the best price.

“At the very least, put the house on your local MLS [multiple listing service] through a flat-fee listing agency,” says Faccone. “You’ll still be responsible for the commission to the buyer’s agent, but by reaching more potential buyers, you’re apt to get a higher price.”

Also, in this era of bidding wars, having an agent at your side is a huge help. Navigating a flurry of “highest and best offer” bids is tough for a rookie!

7. Spacing out on the new place

So you’re all set to sell your house—great! Now, what’s your next move? Avoid winding up with an anxious buyer on one hand and no place to go on the other.

“It can be hard to find the right new home now, so start searching immediately once your property comes to the market,” Reishman says.

“Then be sure to negotiate an extended closing or leaseback, or even make the sale contingent upon purchasing another home.”

If all else fails, line up a rental. Rental market is Super HOT too.

8. Assuming this hot market will last

Inexperienced sellers may turn down a worthy offer or even forestall listing their home, hoping prices will continue to go up. While it may take a while for the seller’s market to top out, interest rates are expected to creep up this year, which could reduce the pool of hungry buyers.

Take away from this article is #TimeToBuy and #TimeToSell is NOW!

{Article source is Realtor.com}

Residential median sales prices posts increase

The final week of February saw a 3% weekly increase in median residential sales prices across MRED's marketplace. The rise to nearly $280,000 also marked a 6% annual bump.

Info source is "Weekly Market Snapshot"

New listings start heating up Feb 2022

The week of Feb.14 brought the largest total of new residential listings in MRED's marketplace since early November. A 14% week-over-week increase in this key metric accompanied a 5% annual bump.

Thank you MRED!

Total active residential listings reach 2022 high

The total number of active residential listings in connectMLS increased to 38,832 during the second week of February. That was a 1.6% week-over-week increase and marked the largest total of the year.

Data source {Weekly Market Snapshot}

#TimeToBuy is now!!!! #ColeSvetlana #ChicagoRealEstate #CRRRealtor

Happy Valentine's Day!

Happy Valentine's Day!

Let's celebrate this season of love!

Keep close those you care about the most!

Sincerely,

LanaCole

#SvetlanaCole #HappyValentine Day! #celebrateLove

Annual market report 2020-2021

- The inventory of homes for sale remained low, as home seller activity did not rise proportionally to meet this demand.

- The number of homes available for sale in 2021 was lower than in 2020 by 33.6%.

- On average, sellers received 98.5% of their original list price at sale, a 2.5% year-over-year increase

- Detached Single-Family home prices were up 14.7% compared to the previous year. Attached Single-Family home prices were up 11.6%.

Source {InfoSparks data}

Closed listings in MRED's marketplace tops previous year

Closed residential listings in MRED's marketplace increased by 10% during the last week. That bump resulted in the first time in six weeks that the current year closed listing total was more than the previous year.

1st week of February 2022 Data.

Source {MRED data}

"How to appeal your property tax."

We just entered into Tax Appeal Season.

Tax appeals can be filed only once a year in a particular time, that is different in every township.

It is a very short time window and it is being changed yearly. You cannot file an appeal once you miss that deadline.

Your property taxes might seem high to you, but that is not a reason for appeal. If you live in a house similar to every other house in the neighborhood, but paying higher property tax than other people in your area who live in similar homes, then you might have grounds for an appeal.

First you need to identify your county, then your township. You also must know your PIN (property identification number). All that is very easy to find on your tax bill. When you know all the needed info you will need to go to your assessors website and print out “soft Tax appeal form”

It will be slightly different for each county and township.

Please note that tax appeal information and directions are not very clear and are hard to find on township sites.

There are 2 ways to go about property tax appeal:

1. By yearly tax amount

2. By assessed property value

Your chances are much higher on succeding when you can show evidence of both of those being too high on your home.

Follow all instructions on how to fill appeal forms out. You also will need to supply min 3 comparable homes in your immediate area proving that those homes pay less tax and that they are assessed higher. Or show comparable of 3 most recent home sales in the area, that sold below assessed value. Both will be ideal!

I attached current tax appeal form for Bloomingdale Township.

You also can hire a tax attorney and let him/her do all the work. They usually charge you half of the amount that they reduce your taxes by.

Happy Tax Season!

"Buying is Now 37.7% Cheaper Than Renting in the US"

The results of the latest Rent vs. Buy Report from "Trulia" show that homeownership remains cheaper than renting with a traditional 30-year fixed rate mortgage in the 100 largest metro areas in the United States.

The updated numbers actually show that the range is an average of 17.4% less expensive in Honolulu (HI), all the way up to 53.2% less expensive in Miami & West Palm Beach (FL), and 37.7% nationwide!

Other interesting findings in the report include:

Interest rates have remained low, and even though home prices have appreciated around the country, they haven't greatly outpaced rental appreciation.

Home prices would have to appreciate by a range of over 23% in Honolulu (HI), up to over 45% in Ventura County (CA), to reach the tipping point of renting being less expensive than buying.

Nationally, rates would have to reach 9.1%, a 145% increase over today's average of 3.7%, for renting to be cheaper than buying. Rates haven't been that high since January of 1995, according to Freddie Mac.

Bottom Line:

Buying a home makes sense socially and financially and I am here to help you!

(Source: http://www.keepingcurrentmatters.com)

Happy coming Holidays!!!!!

"4 Tips for Successful offer!"

So you've been searching for that perfect house to call a 'home' and you finally found one!

The price is right, and in such a competitive market you want to make sure you make a good offer so that you can guarantee your dream of making this house yours comes true!

Freddie Mac covered "4 Tips for Making an Offer" in their latest Executive Perspective.

Here are the 4 Tips they covered along with some additional information for your consideration:

1. Understand How Much You Can Afford

"While it's not nearly as fun as house hunting, fully understanding your finances is critical in making an offer."

This 'tip' or 'step' really should take place before you start your home search process.

As we've mentioned before, getting pre-approved is one of many steps that will show home sellers that you are serious about buying, and will allow you to make your offer with the confidence of knowing that you have already been approved for a mortgage for that amount. You will also need to know if you are prepared to make any repairs that may need to be made to the house (ex: new roof, new furnace).

2. Act Fast

"Even though there are fewer investors, the inventory of homes for sale is also low and competition for housing continues to heat up in many parts of the country."

According to the latest Existing Home Sales Report, the inventory of homes for sale is currently at a 4.7-month supply.

This is well below the 6-month supply that is needed for a 'normal' market. Buyer demand has continued to outpace the supply of homes for sale, causing buyers to compete with each other for their dream home.

Make sure that as soon as you decide that you want to make an offer, you work with your agent to present it as soon as possible.

3. Make a Solid Offer

Freddie Mac offers this advice to help make your offer the strongest it can be:

"Your strongest offer will be comparable with other sales and listings in the neighborhood.

A licensed real estate agent active in the neighborhoods you are considering will be instrumental in helping you put in a solid offer based on their experience and other key considerations such as recent sales of similar homes, the condition of the house and what you can afford."

Consider ways of making your offer stand out!

Many buyers write a personal letter to the seller letting them know how much they would love to be the new homeowners.

Your agent will be able to help you figure out if there are any other ways your offer could stand above the rest.

4. Be Prepared to Negotiate

"It's likely that you'll get at least one counteroffer from the sellers so be prepared.

The two things most likely to be negotiated are the selling price and closing date.

Given that, you'll be glad you did your homework first to understand how much you can afford.

Your agent will also be key in the negotiation process, giving you guidance on the counteroffer and making sure that the agreed-to contract terms are met."

If your offer is approved, Freddie Mac urges you to "always get an independent home inspection, so you know the true condition of the home.

If the inspection uncovers undisclosed problems or issues, you can typically re-negotiate the terms or cancel the contract."

Bottom Line

Whether buying your first home or your fifth, having a local real estate professional who is an expert in their market on your side is your best bet to make sure the process goes smoothly.

(source: http://www.keepingcurrentmatters.com)

Do not hesitate to call me with your questions! I am here to serve You!

Happy House Hunting!

"2 Myths About Mortgages That May Be Holding YOU back"

Fannie Mae's "What do consumers know about the Mortgage Qualification Criteria?"

Study revealed that Americans are misinformed about what is required to qualify for a mortgage when purchasing a home.

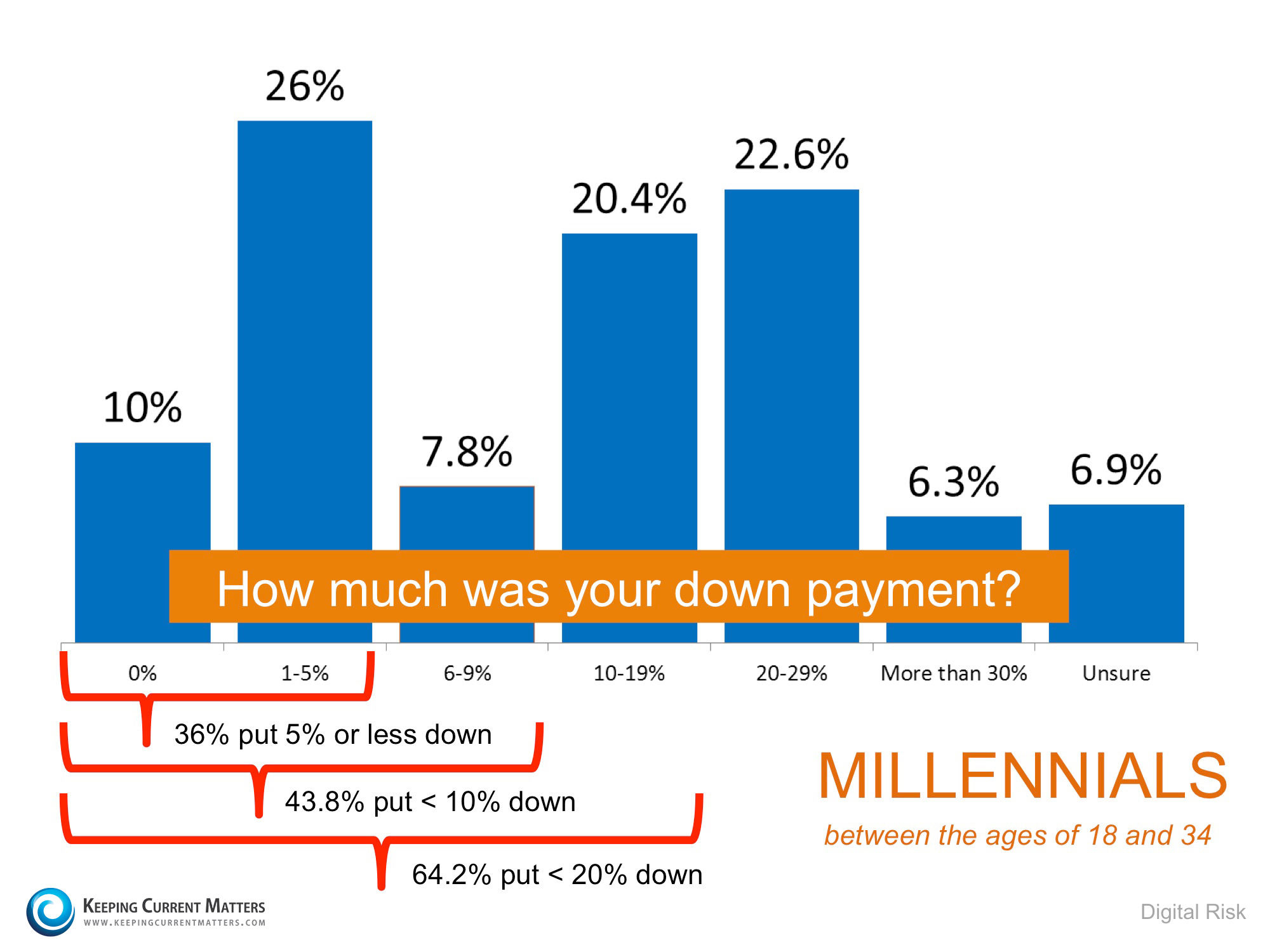

Myth #1: "I Need a 20% Down Payment"

Fannie Mae's survey revealed that consumers overestimate the down payment funds needed to qualify for a home loan.

According to the report, 76% of Americans either don't know (40%) or are misinformed (36%) about the minimum down payment required.

Many believe that they need at least 20% down to buy their dream home.

New programs actually let buyers put down as little as 3%.

Below are the results of a Digital Risk survey of Millennials who recently purchased a home.

As you can see, 64.2% were able to purchase their home by putting down less than 20%, with 43.8% putting down less than 10%!

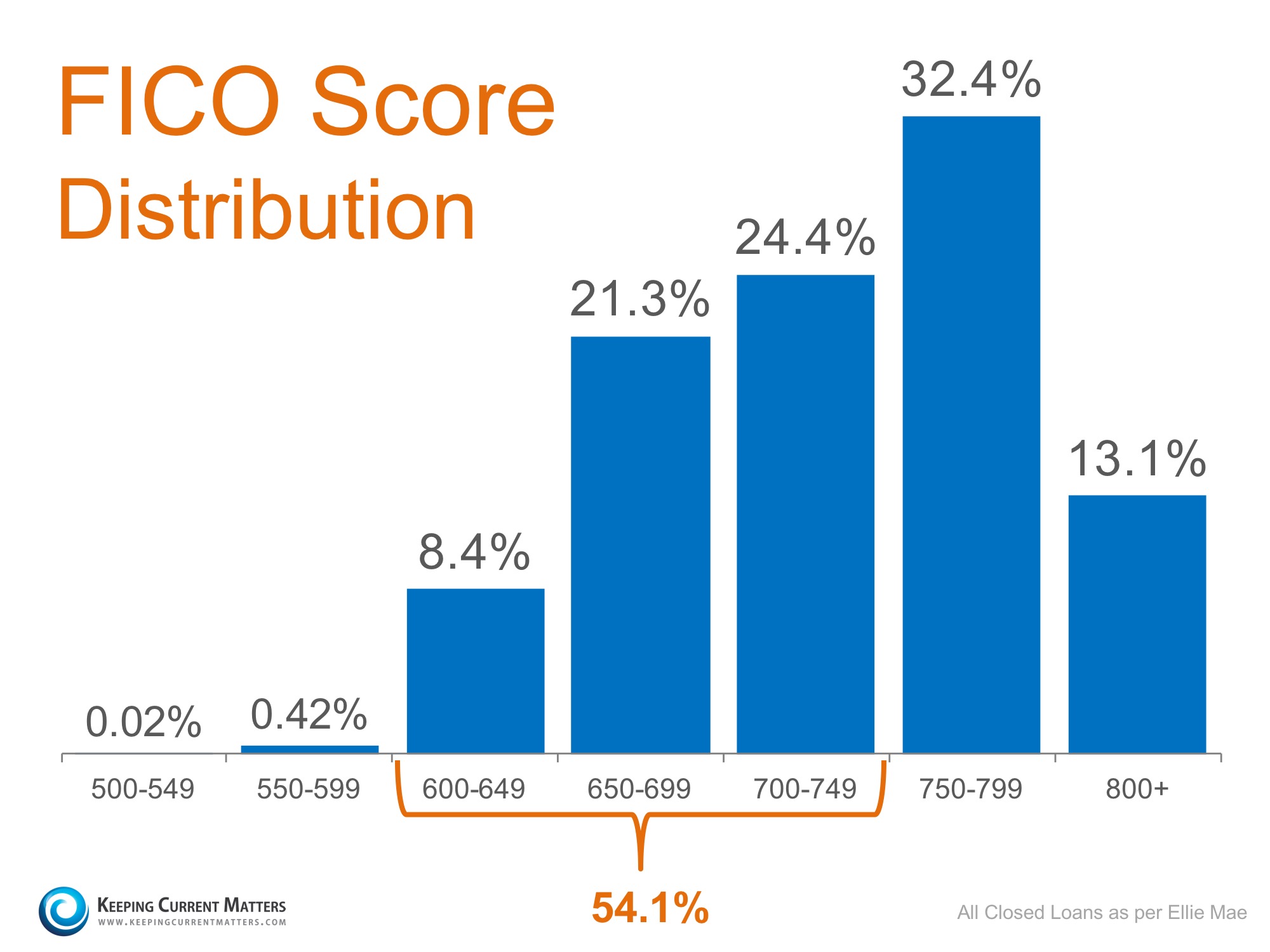

Myth #2: "I need a 780 FICO Score or Higher to Buy"

The survey revealed that 59% of Americans either don't know (54%) or are misinformed (5%) about what FICO score is necessary to qualify.

Many Americans believe a 'good' credit score is 780 or higher.

To help debunk this myth, let's take a look at the latest Ellie Mae Origination Insight Report, which focuses on recently closed (approved) loans. As you can see below, 54.1% of approved mortgages had a credit score of 600-749.

Bottom Line

Whether buying your first home or moving up to your dream home, knowing your options will definitely make the mortgage process easier.

Your dream home may already be within your reach.

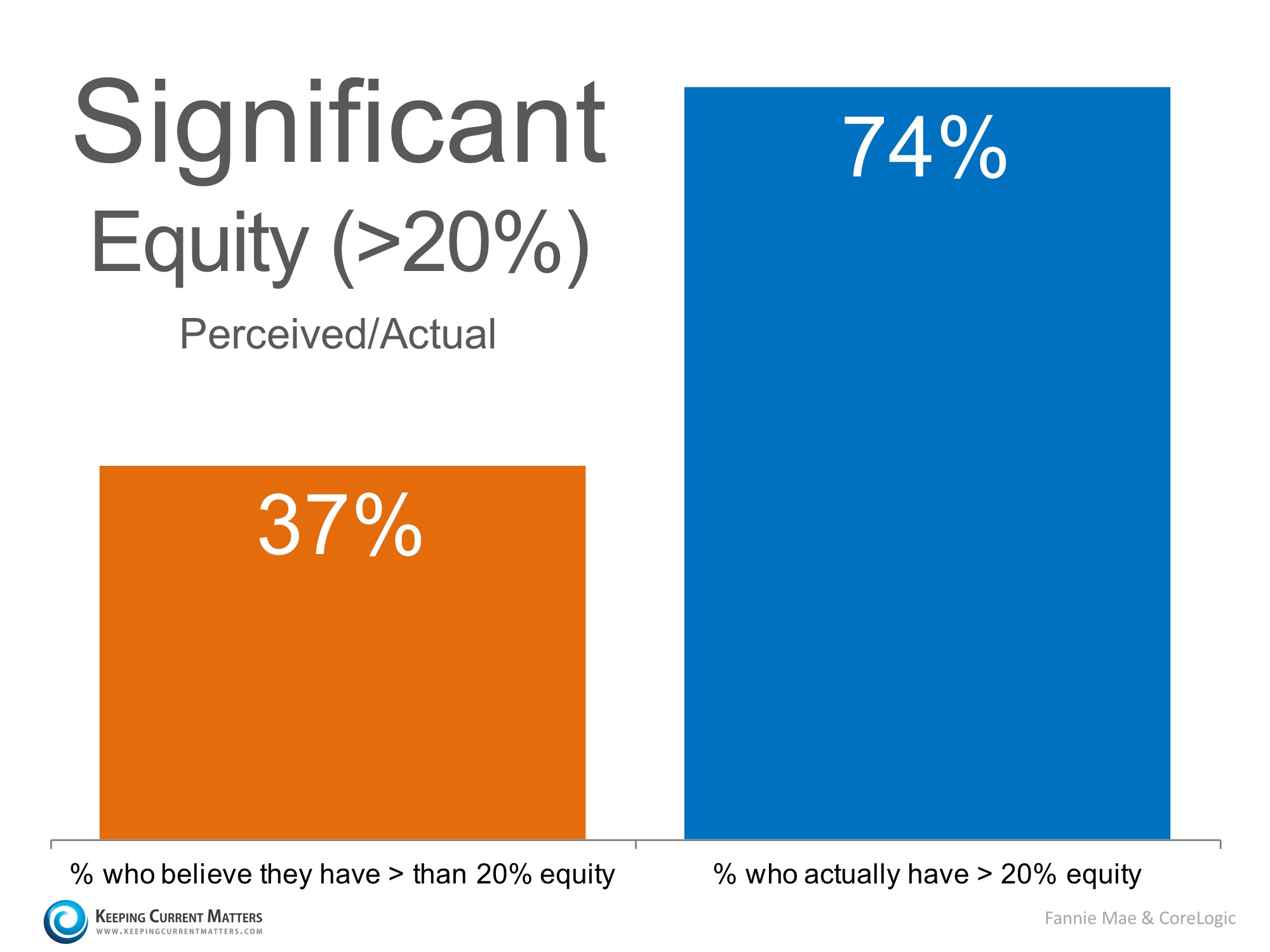

"How much equity is in Your home?"

As of yesterday, CoreLogic's latest Equity Report came out as nearly 268,000 homeowners regained equity and are NO longer underwater on their mortgage in the first quarter.

Homes with negative equity have decreased by 21.5% year-over-year.

A study by Fannie Mae suggests that many homeowners are not aware of how their equity position has changed as their home has increased in value.

For example, their study showed that 23% of Americans still believe their home is in a negative equity position when, in actuality, CoreLogic's report shows that only 8% of homes are in that position.

(Source http://www.keepingcurrentmatters.com/)

The study also revealed that only 37% of Americans believe that they have "significant equity" (greater than 20%), when in actuality, 74% do!

This means that 37% of Americans with a mortgage fail to realize the opportune situation they are in. With a sizable equity position, many homeowners could easily move into a housing situation that better meets their current needs (moving to a larger home or downsizing).

Fannie Mae spoke out on this issue in their report:

"Homeowners who underestimate their homes' values not only underestimate their home equity, they also likely underestimate: 1) how large a down payment they could make with their home equity, 2) their chances of qualifying for mortgages, and, therefore, 3) their opportunities for selling their current homes and for buying different homes."

CoreLogic's report also revealed that if homes were to appreciate by an additional 5%, over 800,000 US households would regain positive equity.

Bottom Line If you are one of the many homeowners who is unsure of your current equity situation and would like to know your options,

contact me and I will be happy to provide you with your Property Value report.

The Best time to Sell is Now!

"Want to buy a home right after short sale?"

You CAN do it now. No need to rent and through your money away while waiting for your credit to improve.

You can apply for a loan just 30 days after short sale. Below you will find a Quick Comparison chart.

Yes, your interest rate will be higher, but you always have an option of refinancing once your credit score has improved. You can work on improving it while living in your OWN home.

Be prepared for a longer closing time - about 60 days.

If you have additional questions please call your Lender.

If you decide to buy, call me!

"Remodel or Not, When to Sell, How to use Psychological price."

Remodel or Not!

We all know to get our home de-cluttered, cleaned and painted in neutral colors before putting it on the market.

But not many of us know what projects will bring us MORE money and which will NOT.

Recent studies (done by Zillow) confirmed that remodeling your bathroom (making it more functional) will bring you more money than remodeling your kitchen (just changing the style of it).

According to Zillow's data a mid-range $3,000 bathroom remodel results in a $1.71 increase in home value for every $1.00 spend on renovation.

{Source :Yahoo.news}

Converting a bedroom into Office - will decrease the value of your home. Buyers like more bedrooms and more space. They have their own imaginations and plans on what they will change in their new home.

Stay within the neighborhood level! Compare your home with other houses in the neighborhood. If your home is significantly upgraded beyond those of comparable homes, you will likely have a harder time recouping your investment, but faster time getting it under the contract.

Check your permits!

Make sure ALL additions and projects were done with proper permits. Have them ready and available or even give copies to your Realtor during listing appointment.

Low quality additions that have been done by unqualified builders, or without permits and approvals will cause problems later when it comes time to sell.

If a would-be buyer has the home inspected and the inspector finds flaws in load-bearing members, plumbing, or electrical systems, it could cause questions to form in the mind of the buyer as to the integrity of the entire home.

Best time to sell!

Home sales reach their peak in June, during the last week of the month residential real estate transactions are 40% higher than average. But when is the right time to list your home?

Best listing time starts in February, but to get the MOST MONEY for your home you should plan to list your house during the last two weeks of March. There's a sharp spike in visitors making contact with real estate agents on Zillow beginning in mid-April and continuing into July.

Selling in the last weeks of March, before the peak in agent contacts and after the peak of newly listed homes in February puts your home in the sweet-spot where it's likely to be seen quickly and not get lost within a flood of new listings.(Per Zillow's tracking analitics)

How to price your home.

Your realtor should present you with "clear and vivid" picture of your neighborhood statistics on homes on the market and recently Sold.

Taking those numbers in consideration and also condition, upgrades and geographical location of your home you and your realtor will arrive to the Fair marketing price.

Little trick or "Psychologically priced" tip!

Ending your home price in a '9' is very beneficial! "If you were going to sell your house for $150,000, just pricing it down by $1000 and selling it for $149,000 ends up in you making $2175 more than you would if you priced it at $150,000." The '9' dynamic works for houses at all price-points.

In the majority of cases, home prices that end in a '9' sell for more for a home of the same relative value that ends in a '0.' The risk that the seller takes on by cutting their home price by $1,000 usually results in gaining more than $1,000 over asking.

Psychological pricing also sold home faster-- Zillow found that homes using '9' in the thousands digit sold four days to one-week faster than those that didn't. {Per chief economist of Zillow Stan Humphries, Source : http://finance.yahoo.com/news/3-tips-for-saving-money-on-your-home-125820548.html}

If you know someone who is looking to buy or sell a home in the next year, please share this News Letter with them!

"Know your Home buying cost!"

READY to buy a house, but not sure what your cost will be?

Here is summary of what to expect and be prepared for.

Education is your power!

Besides the price of the home, there are other costs that need to be paid for a closing, especially where the buyer is getting a loan for the purchase of the home.

There are optional costs, and mandatory costs.

"Home inspection" is an optional cost for all home buyers.

The home inspection provides a detailed report on the home's condition and any problems that could affect the property's price.

This includes reviewing the structure, as well as electrical, plumbing, heating and cooling systems.

Cost usually ranges from $200 to $700.

Buyers who are not in the home remodeling business typically benefit from a home inspection, which can reveal severe problems, that will make you want to cancel and buy a different property.

"Attorney fee" This is another optional fee, for people who are not well-versed in the legal technicalities, or the financial details associated with purchasing real estate. Usually around $500, but varies with the property.

"Survey fee" A survey, or legal map of the property, is optional, but if you're buying a home, you can usually get the seller to buy a survey for you, which costs about $400.

"Title expenses" The title company does two things.

First, it gives you an insurance policy, to guarantee that you own the property that you are buying.

You normally get the seller to buy this insurance for you. The costs varies with the home price, but is usually $1,000 or more.

Second, the title company does the "closing" which means that the title company provides the office where the buyer and seller meet, for the closing, and the title company collects the money from the buyer, and pays the seller, and all of the expenses associated with the closing.

This second part of the title company service is usually paid for by the buyer, if you're getting a loan to buy the property, or the payment is split between buyer and seller if you're paying cash for the property.

The costs varies with the home price, but is usually $800 or more.

"Recording fee" is a mandatory fee which will cover the cost of filing your record of ownership of the property, with the government.

This cost is usually $50 to $100.

If you are getting a loan, you will also have to pay another recording fee for your mortgage document.

The rest of the "closing costs" are normally paid by you if you are getting a loan to buy a property.

"Home appraisal" offers estimated market value of your home, often calculated on comparable sales of similar homes |in your community.

Average cost about $500. Lenders require an appraisal.

"Origination fee" "Underwriting fee" "Credit report fee" are usually fees for services that are provided by your lender, and charged to you, the buyer, when you are getting a loan.

The cost usually ranges from .5% to 2% of the loan amount, depending on lender.

"Title endorsements" are fees that are charged by the title company, but required by your lender.

So you pay for them, because your lender wants them. They usually cost between $100 and $500.

There are endorsement charges for updating your title insurance policy, for using an adjustable rate loan, for buying a condominium, for environmental security, etc.

"Termite inspection" determines if the home has pest damage, and the cost usually runs $150.

If you are getting an FHA loan, you will need to pay for this or get the seller to buy it for you.

"PMI" or Private Mortgage Insurance.

If you borrow more than 80% of the purchase price, you will normally have to pay for private mortgage insurance, which can be about $65 per month, for every $100,000 that you borrow.

So your monthly mortgage payment can be over $100 per month higher, because you didn't put down enough money.

And the PMI payments don't go toward the purchase price.

They are insurance payments. Sometimes, you can get charged with a large PMI payment at the beginning, on top of the monthly payment.

Be careful about PMI charges.

There is other money that you need for a closing, but that is not actually an an expense for you.

These are like putting money in the bank. It's your money, but unless it's in the bank, you don't get the home.

"Escrow deposit" is a cost that you will pay if you are getting a loan, and you are borrowing 80% or more of the purchase price.

The bank will require you to put money into an escrow account, that the bank keeps, so that the bank can use the money to pay your property taxes and homeowner insurance.

You will usually need to start the account by putting in 2 months of property taxes, and homeowners insurance. (Plus PMI, discussed above)

"Earnest money" you put down to demonstrate that you're serious about buying the seller's home.

You'll get the money back once you close or you can add it to your down payment.

You decide how much this will be, but usually it's $1,000, up to about 5% of the purchase price.

Note that you also need to plan for additional "after purchase" expenses.

Moving your furniture, paying monthly or annual HOA dues if your neighborhood has a homeowners association, etc.

Once you access all above and feel ready to buy, contact a Mortgage Banker who will help you get pre-qualified for a loan.

You’ll get an estimate of how much you’ll be able to borrow.

You can also use a mortgage affordability calculator to estimate how much you will be able to borrow.

Once you have this useful information you can call your favorite Realtor to enter into the FUN part of the real estate purchase-the house hunt!

Happy hunting!

And do not forget the Best time to buy is NOW!

"Is the most favorable time to buy running out?"

We've been hearing the same story for the past 4 years that the best time to buy is now and that the interest rate is lower than ever now.

So is all that correct?

And how will we know whether now is the time to buy?

Following the history of the sale prices from 2010 to 2014 we can see healthy price increases, while interest rates were not changing much, making home ownership more and more attractive.

House prices are on the rise, but they're still dramatically low and affordable.

Some financial gurus predict interest rates to go up starting late next month due to discontinuation of Stimulus Plans, according to the minutes of the June 17-18 Federal Open Market Committee Meeting.

"All signs point to rates going up in the future" says Brian Koss, executive vice president of Mortgage Network in Danvers, Massachusetts.

"As October approaches, I believe we will begin to see rates edge higher."(source {https://homes.yahoo.com/news/refi-before-october011346078.html})

Higher interest rates mean higher monthly payments, which not only affects new home buyers but also current home owners who want to sell.

Another reason why qualified buyers should not wait is investors.

Thousands of small and big investors popped up everywhere plus US being flooded with foreign investors , who are full of cash and they are snapping up available deals.

The reason is simple - real estate is the BEST investment of their funds right now.

Most of them earn close to zero in banks savings and do not feel comfortable investing in the Stock Market!

Not to mention the rental market profitability that just Exploded during the last 2 years!

Even builders started to feel confident again jumping into new construction!

So those are 3 main reasons WHY Time and Prices are still right!

(Low interest rates, low prices, and emerging competition from investors)

Congratulations to anyone who is able to buy now!

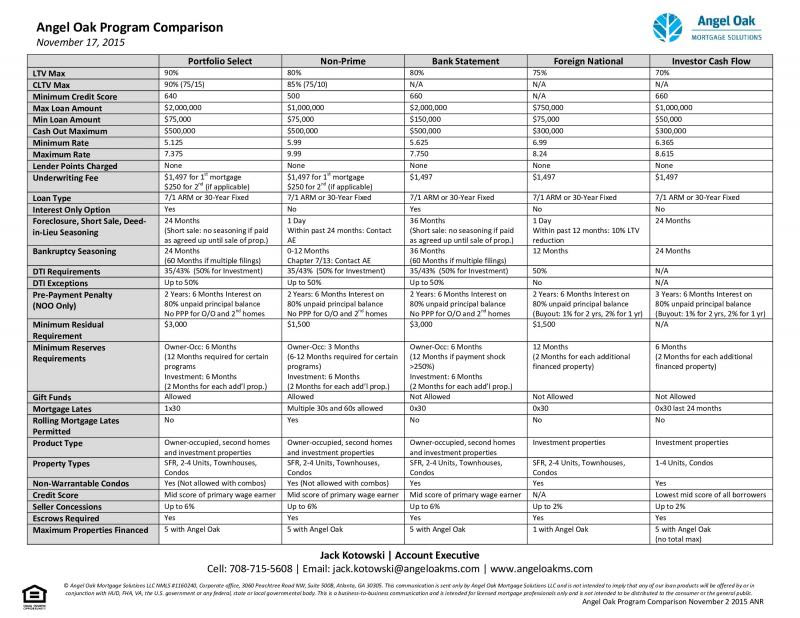

Is House Purchase Financing your next Goal!

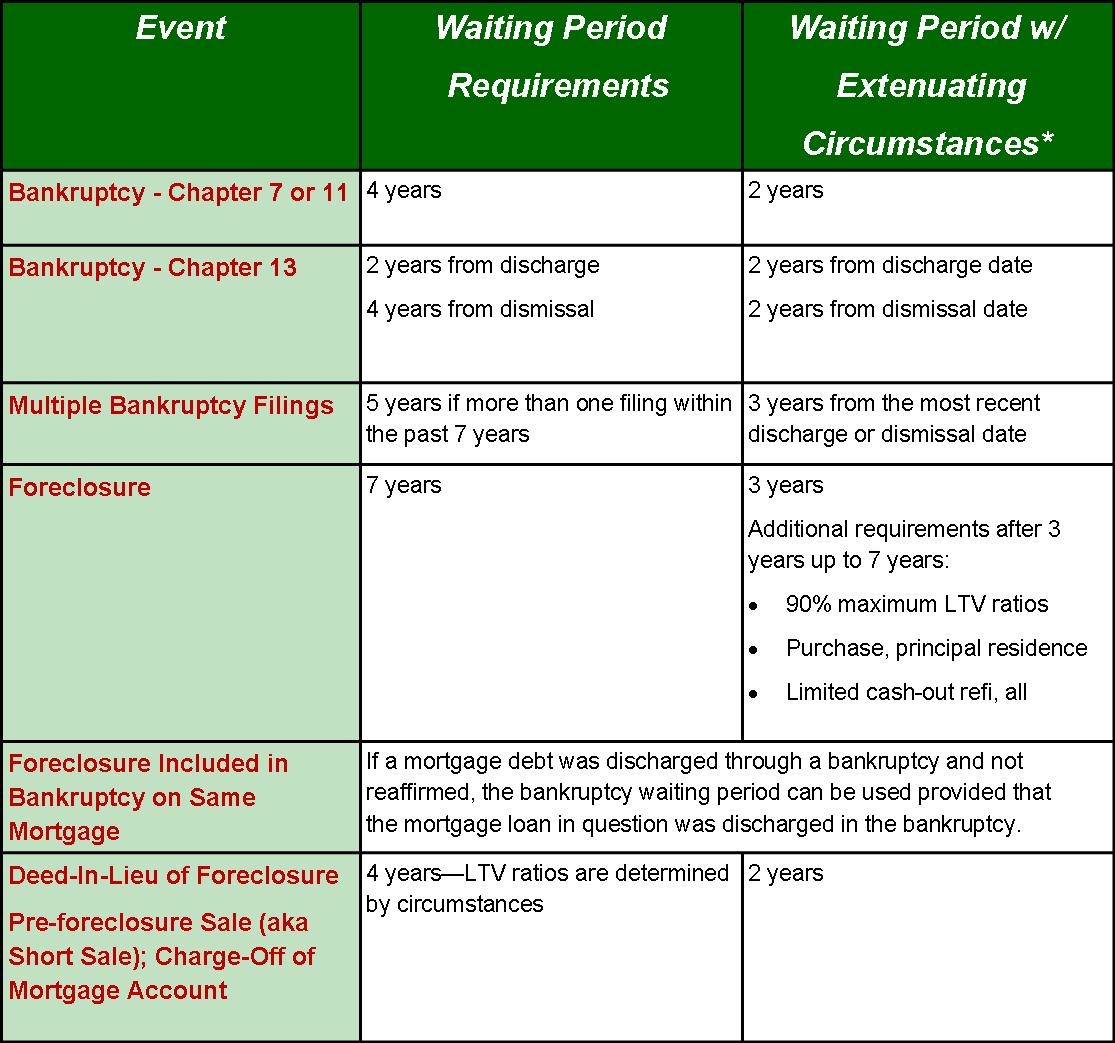

Have you had short sale, foreclosure or bankruptcy in the past?

Wondering when are you eligible to obtain house financing and purchase a home again?

Experiencing a damaging credit event as a foreclosure, short sale, divorce, bankruptcy does NOT mean that you will not be eligible for another mortgage.

You need to know and understand the time line by which lenders establish your eligibility. Knowing this information will help you to prepare yourself for a future successful purchase and to plan your savings for down payment.

Having a knowledgeable real estate agent and lender on your side will help you keep your waiting time to a minimum and make sure that your credit is being repaired.

You can buy short sale or REO homes even after you had one yourself in the past, once you are eligible to borrow again.

There are lots of options out there:

-FHA home loans with low down payment

-FHA 203K construction loan

-203k loan

-Government housing assistance programs for 1st time buyers

-Illinois down payment assistance program with up to $7,500 towards your down payment.

If none of the above apply to you, there are always plenty of houses for sale with owner financing.

In some cases the waiting period for eligibility might be shorter.

If you experienced extenuating circumstances that are beyond your control such as loss of job, death of a wage earner etc.

All such events will require document verification and will be subject to underwriter approval.

Yelp about us:

"Open House VS Internet Marketing"

In your opinion has the Internet Age Open House Become Irrelevant?

In the old days, sellers could rely on open houses to give their properties wide exposure to potential buyers.

But now, thanks to the Internet, the traditional open house is starting to feel like an old approach.

The vast majority of buyers now dip their toes into the housing market online. They can easily narrow their choices through websites with vast databases of local properties for sale.

From there, most buyers turn to real estate agents with the expertise, local knowledge, and access to statistics, to hone in on a few special properties. They might attend an open house, but most prefer individual tours from their agents.

Meanwhile, sellers hope for the kind of response to their open houses that their parents might have received. They're usually disappointed.

These days, sellers are under competitive pressure to stage their properties before open houses. What began as a way to differentiate one property from the rest is now almost mandatory in some neighborhoods. The cost: upwards of $2,000.

For pictures, videos, and personal tours of your home, staging may pay off in faster sales and higher asking prices, but don't count on the staged open house to generate offers. These days, you'll get more browsers than qualified buyers.

And don't hold multiple open houses. Hosting several open houses says "desperation" to buyers and may encourage lowball offers.

What is Real Estate Tax?

Real Estate tax is a complicated matter, but we all have to know WHAT is it and WHY are we paying so much money 2 times a year.

This short video created by Illinois Organization of Realtors explains Tax matter very simple and interactive.

What can we do for you!

Build Wealth Irrespective of Your Current Financial Position!

One Stop Solutions Available HERE!

Are you at the brink of a foreclosure?

Are you struggling to retain your property ownership?

Do you require professional handling of loan modifications?

Would you like to make profits on Real Estate transactions?

Welcome to Chicago-Land-RealEstate.com, and I am Svetlana Cole, your "Doctor-Know-It-All" of real estate solutions!

Often, clients approach me when they face the dead end of the “hope road”, they are either on the brink of bankruptcy or foreclosure.

No doubt, these situations are highly challenging, and require immediate intervention with robust Real Estate skills.

We come to your rescue immediately with the aim to provide:

-Complete professionalism & expertise

-Reliable & honest services

-Full confidentiality & timely responses

Naturally, clients love us and never forget to contact us whether they are looking for property investment or are facing their worst Real Estate issues.

Our Services

We offer a wide range of services at part with the industry standards and unique customer requirements.

This includes:

-Real Estate Buying: Whether you are looking to buy a commercial or a residential property, your main aim is to invest successfully and build an asset. I will help you to make the right decision.

-Real Estate Selling: We offer complete professionalism and passion to help you get the best value for money with your property. We will guide you in the right direction and help you make optimal profits.

-Help with Foreclosure Investment: Are you looking to invest in a foreclosure property? We will help you make the best decision on maximum savings and wealth building opportunities. Make 35% to 53% gross profits on such properties with our guidance!

-Help with Stopping Foreclosures: When you find yourself at the other end of real estate spectrum, there is no need to feel gloomy.

We have helped hundreds of clients fight foreclosure, turning it into a profitable situation with our express help and guidance!

We can help you too!

How It Works?

When you approach Us, we will understand your requirements through in-depth, one-on-one discussion.

In real estate buying and selling, we will work with you right through the end of the tunnel, until you achieve your business transaction.

We will be your friend in need when it comes to stopping foreclosures, which is our forte.

We will help you to turn a negative situation into a profit-making one.

Come to us to understand your foreclosure situation better!

Our Benefits:

-Postpone foreclosure & get enough time to arrange amounts needed

-Receive money from the bank for doing short sale

-Valuable advice that helps you save money

-Comprehensive financial situation analysis

-Best solutions to get wealthy as soon as possible

What’s more, with us you can benefit from our FREE consultations where you can get the best possible professional advice without spending a dime!

So whenever you find yourself in a Real Estate fix, do not delay and make your situation worse.

Contact us instead, to see your problems vanish!

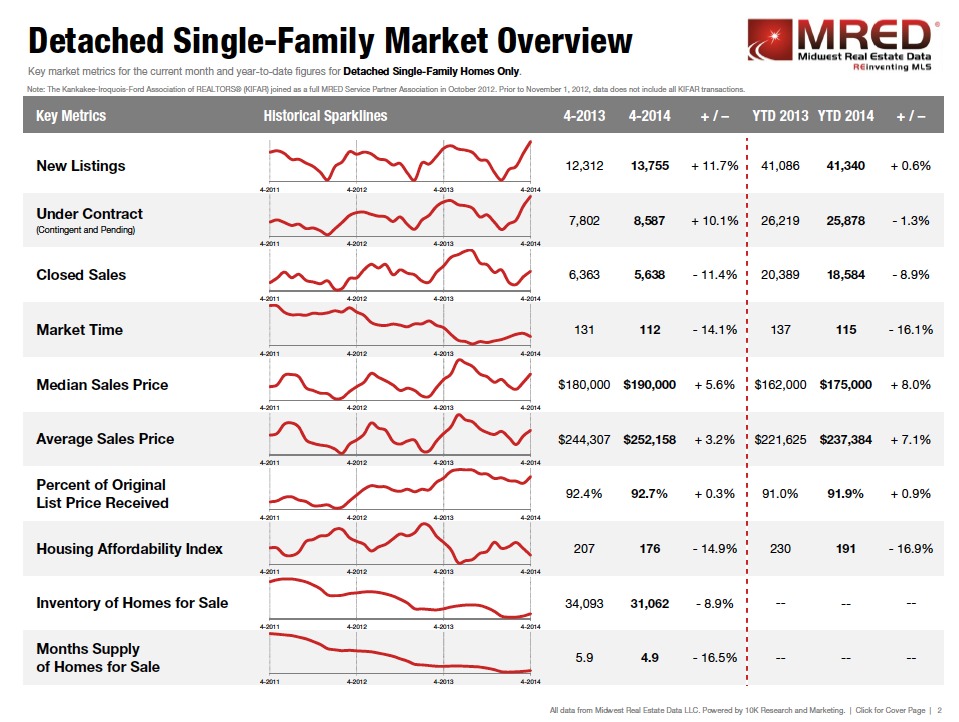

Market Overview

Detached Single Family Market Overview per Realtors confidence index.

NATIONAL ASSOCIATION OF REALTORS®

Research Department

Lawrence Yun, Senior Vice President and Chief Economist

Based on Data Gathered May 2 – 9, 2014

#ChicagoLand NewsLetter #LanaColeRealtor #RealEstateMarket